Protect What Matters.

Partner with IAT for tailored Management Liability coverage.

Business leaders today face a growing set of challenges that increase management liability risk. Inflation, evolving labor laws, remote workforce dynamics, and a shifting claims environment are putting more pressure on businesses. At the same time, fluctuating insurance premiums and capacity are making it harder to secure reliable protection. In this environment, understanding how to manage liability exposure — beyond just focusing on price — is critical to long-term business resilience.

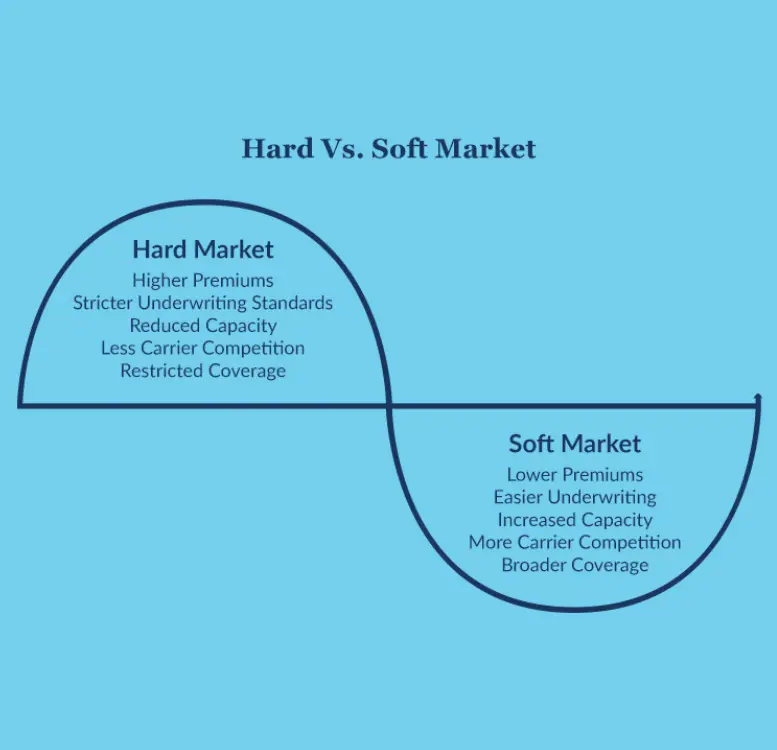

Over the past decade, the management liability insurance market has swung from soft to hard and back again:

Hard Market:

Stricter underwriting standards

Reduced capacity

Restricted coverage

Soft Market:

Lower premiums

Easier underwriting

Increased carrier competition

Broader policy terms

As new carriers enter the market and promise aggressive pricing, your clients may be tempted to shop around. But frequent switching — especially with claims-made policies — can introduce dangerous coverage gaps.

Directors & Officers (D&O) Liability Insurance

Protects executive leadership from personal financial loss due to:

Employment Practices Liability Insurance (EPL)

Covers legal costs and damages stemming from:

Fiduciary Liability Insurance

Protects against claims involving:

Download Now

In times of high interest rates and rising costs, businesses may cut elective coverages like EPL. However, dropping management liability insurance during financial stress can increase risk. Here are key risks of having a coverage gap during financial strain:

Claims-Made Policy Limitations: Most management liability policies (D&O, E&O) only respond to claims made and reported during the policy period. Skipping a policy year creates dangerous gaps, leaving businesses fully exposed to litigation.

Tip: Maintain uninterrupted coverage to avoid exposure.

Inflation-driven financial pressure is forcing companies to make tough decisions, and D&Os are increasingly held liable for revenue loss, cost-cutting missteps, or failed responses to economic stress.

Tip: Help clients document sound decision-making under pressure.

Higher wages + larger workforces = costlier claims.

With more employees in the labor market and average salaries up, EPL claim severity has surged, especially around terminations, discrimination, and pay equity.

Tip: Recommend thorough HR documentation and updated EPL limits.

Claims-Made Policy Limitations: Most management liability policies (D&O, E&O) only respond to claims made and reported during the policy period. Skipping a policy year creates dangerous gaps, leaving businesses fully exposed to litigation.

Tip: Maintain uninterrupted coverage to avoid exposure.

Inflation-driven financial pressure is forcing companies to make tough decisions, and D&Os are increasingly held liable for revenue loss, cost-cutting missteps, or failed responses to economic stress.

Tip: Help clients document sound decision-making under pressure.

Higher wages + larger workforces = costlier claims.

With more employees in the labor market and average salaries up, EPL claim severity has surged, especially around terminations, discrimination, and pay equity.

Tip: Recommend thorough HR documentation and updated EPL limits.